Why Islamic Car Finance is Actually Different from a Conventional Loan — and Why It Matters

Let me be straight with you from the beginning. I sit in an auto finance office in Karachi, and I have this conversation almost every week. Someone walks in, fills out their paperwork, and at some point asks the question they were thinking about the whole time: “Bhai, yeh Islamic finance hai ya sirf naam ka?”

It’s a fair question. Because in Pakistan, we’ve all seen things get the “Islamic” label slapped on them without much changing underneath. So the skepticism is earned. But in the case of car finance specifically — and Diminishing Musharakah in particular — the structure is genuinely different. Not different in a small, technical way. Different in a way that affects what you actually own, what risk you carry, and what happens if things go wrong.

I want to explain it the way I’d explain it to a cousin sitting across from me, not the way a brochure would.

Start here: what a conventional car loan actually is

When you take a conventional car loan from a bank, the transaction is straightforward. The bank gives you money. You go buy a car. You own the car from day one. And then you spend the next 3 to 5 years paying back the bank — with interest on top.

The car is yours. The debt is yours. The bank holds the vehicle’s documents as security, but legally, you are the owner. If the car gets stolen or totaled in an accident, that’s primarily your problem, not the bank’s. The bank still wants their loan repaid.

The profit the bank makes is called interest. It’s a fixed percentage on the money they lent you, and it runs for the entire duration regardless of what happens to the asset. You could run that car into a wall on day two — the bank still gets their interest.

This is what makes it Riba under Islamic law. The bank profits from time and money alone — not from any participation in the asset, any shared ownership, or any shared risk.

Now let’s talk about Diminishing Musharakah — in plain language

Musharakah is an Arabic word that means partnership. Diminishing Musharakah is a partnership that intentionally shrinks over time — until one partner owns everything.

Here’s the story version. Imagine you want to buy a house — or in our case, a car. You have Rs. 7,35,000 saved up, but the car costs Rs. 24,50,000. You’re short by Rs. 17,15,000. You can’t buy it alone.

In a conventional setup: a bank lends you Rs. 17,15,000. You buy the car. You owe the bank Rs. 17,15,000 plus interest. The car is yours; the debt is yours.

In Diminishing Musharakah: you and the bank buy the car together. You contribute 30% (your down payment). The bank contributes 70%. From day one, you both co-own the vehicle — you own 30% of it, the bank owns 70%.

Now here’s what happens every month. You pay the bank two things: a rental for using their 70% share of the car (because you’re driving it, not them), and a purchase installment — buying a small slice of the bank’s share. Every month, your ownership grows and the bank’s ownership shrinks. After 5 years of payments, you’ve bought out the bank’s entire share. The car is 100% yours.

Why this difference is not just philosophical

Here’s where it gets practical. A lot of people assume the Islamic vs conventional debate is purely a religious one — and that if you’re not particularly observant, it doesn’t affect you. That’s not quite right.

The co-ownership structure has a few real-world consequences that have nothing to do with religion.

The bank has a stake in the car’s condition

Because the bank genuinely co-owns the vehicle during the financing period, they have a real interest in the asset being protected. This is why Takaful (Islamic insurance) is included as part of the arrangement — not as an optional add-on, but as a structural requirement. The bank isn’t covering your risk as a favour. They’re covering their own asset.

Think of it like renting a flat with a friend. If the flat gets flooded, it’s both your problem — not just yours. The bank’s motivation to ensure the car is insured and protected is genuine, because they own a piece of it.

The rental reduces as your ownership increases

This is subtle but important. In Diminishing Musharakah, your monthly rental should theoretically decline as you buy more of the bank’s share. Because if you own 50% of the car, you’re only renting the bank’s 50% — not their original 70%.

In practice, Islamic banks in Pakistan use a fixed installment structure (calculated via PMT formula on the finance amount), but the Takaful component does decline year on year — because it’s calculated on the declining outstanding balance. Your Year 5 total payment is genuinely lower than your Year 1 total. The bank covers Takaful in the final year entirely.

Early settlement works differently

In a conventional loan, when you pay off early, you’re retiring a debt. There may be early settlement penalties tied to the expected interest income the bank loses.

In Diminishing Musharakah, when you pay off early, you’re buying out the remaining share of the bank’s ownership. The bank loses future rental income on a share they no longer own. The calculation is fundamentally different — and in many cases more transparent, because it’s based on remaining ownership, not projected interest curves.

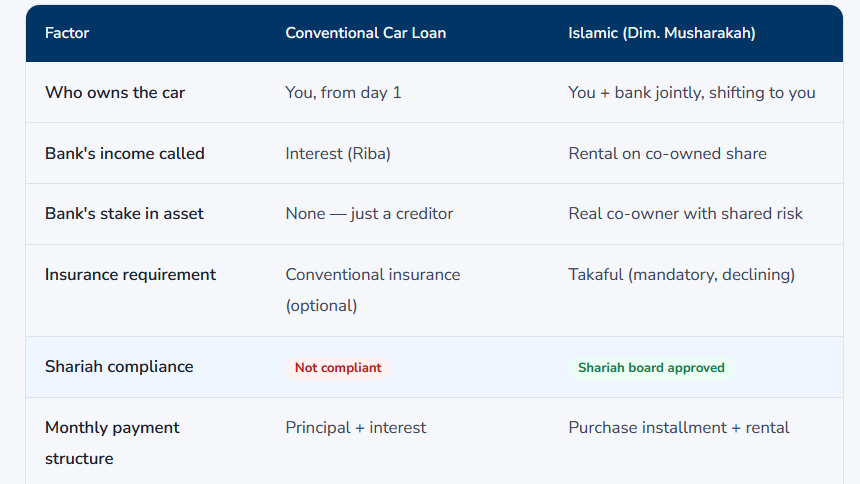

The honest comparison — Islamic vs conventional, side by side

| Factor | Conventional Car Loan | Islamic (Dim. Musharakah) |

|---|---|---|

| Who owns the car | You, from day 1 | You + bank jointly, shifting to you |

| Bank’s income called | Interest (Riba) | Rental on co-owned share |

| Bank’s stake in asset | None — just a creditor | Real co-owner with shared risk |

| Insurance requirement | Conventional insurance (optional) | Takaful (mandatory, declining) |

| Shariah compliance | Not compliant | Shariah board approved |

| Monthly payment structure | Principal + interest | Purchase installment + rental |

| Early settlement | Debt repayment + penalty | Ownership buyout (cleaner) |

| Rate benchmark | KIBOR + margin | KIBOR + margin (same benchmark |

The question everyone actually wants answered: is it cheaper?

Honestly? At the headline rate level, Islamic and conventional car finance in Pakistan cost roughly the same. Both use KIBOR as their benchmark. Islamic Banks usually charge KIBOR + 5% for salaried customers on new vehicles. A conventional bank might charge the same. The profit margin the bank earns is comparable.

So if you’re purely looking at the monthly installment figure — the base number is similar.

But total cost of ownership tells a slightly different story when you factor in the Takaful structure. In a conventional loan with comprehensive insurance, you pay a fixed premium throughout. Under Diminishing Musharakah, Takaful is calculated on the bank’s declining ownership share — so it reduces each year. By Year 5, the bank covers the Takaful entirely. That’s a real saving, even if it sounds small in isolation.

“The base installment is comparable. But when you add up the Takaful savings over 5 years, Islamic finance works out meaningfully cheaper in total — especially for smaller cars on longer tenors.”

What Diminishing Musharakah is not

I want to address a misconception directly, because I hear it often. Some people believe Islamic banking is just conventional banking with the word “interest” replaced by “profit.” The suggestion is that it’s window dressing — that underneath, the math is the same and the bank makes the same money.

The math at a surface level does produce similar monthly numbers. That’s true. But the structure underneath is different, and that structure matters for three reasons.

First, the nature of the transaction is different. A loan creates a debtor-creditor relationship. Musharakah creates a co-owner relationship. These have different legal implications, different risk-sharing implications, and different moral implications if you believe those things matter.

Second, the bank’s incentive is different. A conventional lender doesn’t care what happens to your car — they just want their loan repaid. An Islamic bank, as a genuine co-owner, has a structural reason to care about the asset’s condition and protection. That’s not just theory — it’s reflected in the mandatory Takaful requirement.

Third, the Shariah scholars who review these structures are not naive. Pakistan’s Islamic banks are reviewed by Shariah boards that include serious scholars. They are not in the business of approving the same thing twice with different labels. If they certify Diminishing Musharakah, it’s because the structure passes substantive scrutiny — not just a name change.

A real conversation I have almost every week

A customer came in last month — mid-thirties, government job, decent salary. He wanted to finance a Suzuki Cultus. He’d done his research online and arrived with a printed rate comparison from a conventional bank and from us.

On the surface, the monthly installment from the conventional bank was Rs. 200 lower. He was leaning toward them.

I walked him through three things. One: the conventional bank’s insurance premium was fixed at 2% of vehicle value per year. Our Takaful starts at 1.5% and declines. Over 3 years, that’s a genuine saving. Two: as a filer, his WHT obligation was zero with us and with them — so that was a wash. Three: the conventional bank had a Rs. 3,000 per month early settlement penalty clause that he hadn’t noticed in the fine print. We don’t.

By the end of the conversation, the total cost over 3 years was actually lower with us — not dramatically, but lower. And he left with a car financed on a structure he felt comfortable with.

I’m not telling this story to sell you on Faysal Bank specifically. I’m telling it because the comparison is rarely as straightforward as the headline installment number. You have to look at the full picture.

So should you choose Islamic car finance?

If you’re a Muslim and Riba concerns you — yes, unambiguously. Diminishing Musharakah is structured to avoid the core objection to interest-based lending. It’s been scrutinised by scholars, not just lawyers.

If you’re not religious but you’re analytical — compare the total cost over the full tenor, including insurance/Takaful, any early settlement clauses, and the structure’s transparency. Islamic finance often holds up well under that analysis.

If you’re purely looking for the lowest possible monthly number and nothing else — both options are worth getting exact quotes on, and the difference will likely be small.

What I’d tell anyone sitting across from me is this: don’t just look at the number in the “monthly installment” box. Look at what you’re actually entering into. A loan is a debt. Musharakah is a partnership. Those are not the same thing — and for a lot of people, that distinction matters.

Every article on this site comes from direct experience in the field — not from research papers or copied brochures. I’ve processed hundreds of car finance applications across Sindh, and the questions I answer here are the ones real customers ask me every week.